CPA FRM - Module 2: Management of liquidity, debt and equity | KnowledgEquity

- Oct 30, 2020

- 6 min read

At the end of this module, you should be able to:

explain and apply the concepts of cash flow and working capital management

discuss how capital structures are determined using a simplified structure of debt, equity and preference shares

calculate the cost of debt, ordinary shares (equity) and preference shares and explain the capital asset pricing model (CAPM)

calculate and use the before- and after-tax weighted average cost of capital (WACC).

Part A: Cash flow management

Which of the following is considered to be a cost associated with maintaining liquidity?

Interest earned on invested surplus cash

Finance facility costs for unused financing facilities

Margin costs on borrowings due to poor credit rating

A.1. Liquidity risk

Not being able to:

meet obligations as and when they fall due

convert assets into cash quickly without material price reduction

How do you measure liquidity

current ratios = current assets / current liabilities (1.5 - 2)

quick ratio = current assets - inventory) / current liabilities (1 - 1.5)

A.2. Cash management

forecasting and planning

cash procedures

inter-company transactions

investing surplus funds

monitoring and measuring performance

A.3. Cash disbursement

timely and accurate payments

policies and infrastructure

authorization

segregation of duties

record-keeping

independent check

A.4. Free cash flow

underlying cash generated by their business:

operating cash flow

less capital invested

after-tax cash flows available to capital providers

[net income + depreciation and amortization - changes in net working capital - capital expenditure]

net income: accrual basis, after tax

depreciation and amortization: non-cash item, relates to prior period outflows

changes in net working capital: reflects the growth of the organization

capital expenditure: no longer available to external providers

Example A.4.1

net income + depreciation and amortization - changes in NWC - CapEx

50,000 + 20,000 - 25,000 - 20,000 = 25,000

A.5. Stress testing

Part B: Working capital management

B.1. Strategies to manage working capital

B.2. Measuring working capital requirements

B.3. Funding risk and credit risk assessment

need to consider the "cash effects"

assets

liabilities

tax effects (e.g. interest/ depreciation / amortization)

Example B

Delicious chocolate supplies boxes of chocolates to a supermarket:

purchases on credit, payable within 30 days from supplier invoice date

inventories sold after 50 days

sales are on credit, payable 60 days from invoice date

Days between outflow of cash and inflow of cash: 50 + 60 - 30 = 80 days

Working capital drivers

inventory cycle

receivable cycle

payable cycle

Cash cycle & Operating cycle

Pre-webinar activity

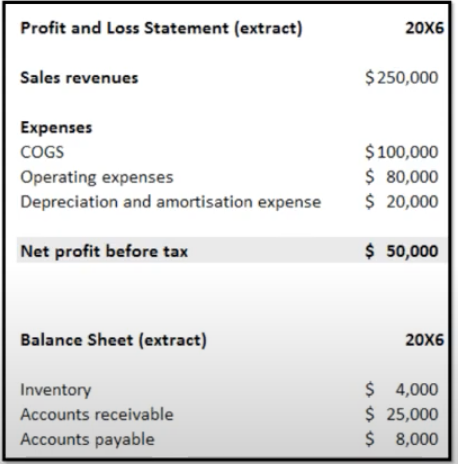

What is the 20X6 cash conversion cycle:

CCC = Days of Sales Outstanding (DSO) + Days of Inventory Outstanding (DIO) - Days of Payables Outstanding (DPO).

DSO = [(BegAR + EndAR) / 2] / (Revenue / 365)

= $25,000 / ($250,000 / 365) = 36.5 days

DIO = [(BegInv + EndInv / 2)] / (COGS / 365)

= $4,000 / ($100,000 / 365) = 14.6 days

Operating Cycle = DSO + DIO

= 36.5 + 14.6 = 51.1 days

how many days it takes for something to go from first being in inventory to receiving the cash after the sale. You want this number to be low meaning that merchandise isn’t sitting on shelves too long and customers are paying relatively quickly. https://blogs.cfainstitute.org/insideinvesting/2013/05/21/a-look-at-the-cash-conversion-cycle/

DPO = [(BegAP+EndAP) / 2] / (COGS / 365)

= $8,000 / ($100,000 / 365) = 29.2 days

how many days the company takes to pay its suppliers. Unlike the other two numbers that make up the Operating Cycle, the company wants to stretch out how long it takes to pay for its inventory.

Cash conversion cycle = 51.1 - 29.2 = 21.9 days

What advice can you give?

ask suppliers to increase the terms of engagement or the credit days (to extend payable days)

ask or force customers to pay early (to reduce receivable days)

there's a risk that the organization could lose some customers or critical suppliers

Part C: Cost of capital and capital structure

e.g. Blendle

Pay-per-article journalism start up:

initial high investment in infrastructure and running costs

costs associated with ramping up agreements with publishers

low initial income, and hard to forecast income/growth

e.g. NAB

Listed multi-national financial institution:

Significant capital and IT infrastructure in place

Operating costs have a long history

Funding costs can fluctuate based on international markets

Income largely based on margins/spreads and fees (reliant on number of clients/transactions)

Capital structure

C.1.Qualitative factors

Underlying asset structure - generating 'predictable cash flows'

Earnings stability

Flexibility required (debt is more flexible)

Management control (equity)

Risk profile

Cost (deb cost is lower)

Imposed constraints (e.g. debt covenant)

Quantitative factors

Cost of debt

Cost of equity

Cost of preference shares

Weighted average cost of capital (sum of everything above)

Quiz C

Crafty Metal issues a one-year bond with a face value of $200,000 and a coupon rate of 7%.

The current market price for the bond is $198,148.

What is the cost of debt?

cost of debt = [(coupon payment + face value) / market price] - 1

[( 200,000 + 14,000) / 198,148] - 1

( 200,000 x 1.07 ) / 198,148] - 1 = 8%

Market price of debt security

coupon payments: the amount you'll be getting over the period of the bond, as interest on that bond

every bond will have a certain percentage so if it's a fixed interest security it might say 4% on the face value and you'll always get that

PV of the face value repayment: at the end of the term of the bond that amount has to be refunded back or paid back - to whoever has invested in the bond

P0: present value

C: coupon payment

kd: market yield

Fn: face value

A 3-year bond with a face value of $100,000 and market yield of 4% carries a coupon of 6% per annum paid annually

P0 of coupon payments = [($6,000/0/04)(1-1/(1+0.04)^3] = $16,650.55

P0 of face value repayments = [$100,000/(1+0.04)^3] = $88,899.64

P= $105,550.19

A 3-year bond with a face value of $100,000 and market yield of 4% carries a coupon of 6% per annum paid semi-annually

P0 of coupon payments = [($3,000/0/02)(1-1/(1+0.02)^6] = $16,804.29

P0 of face value repayments = [$100,000/(1+0.02)^6] = $88,797,14

P= $105,601.43

market price is how much you could be able to sell this bond

Cost of debt

coupon rates are not the cost of debt (although they can be the same in some situations)

if coupon rate < cost of debt, then market price < face value (vice versa)

E.g.

coupon rate: 4%

cost of debt: 6%

meaning, you are stuck with this 4% fixed history Interest security, whereas in a market you could have gotten 6%. Therefore, the market price of that bond will be less than its face value.

Cost of equity

= shareholders

unsystematic risk = very inherent to that company

assumed to be removed through diversification of a portfolio

Does the capital asset pricing model use systematic risk or unsystematic risk?

systematic risk, because the CAPM assumes that you have a well diversified portfolio

CAPM specifies the relationship between a security's systematic risk and its required return

Risk-free interest rate: equivalent to government Treasury bond - risk of default is really low

Expected return on market portfolio: you will tend to expect a higher return than a risk-free interest rate

Expected market risk premium: difference between the expected return and the risk-free rate

Beta: systemic risk that cannot be diversified away (inherent in the market)

Assume the cost of equity for ZYX is 16.5%

1. If the risk-free interest rate is 3% and the market risk premium is 9%, what is the beta for ZYX?

ke = rf + market risk premium x β

16.5% = 3% + [9%] x β

13.5%/ 9% = β

β = 1.5

2. What would be the cost of equity for ZYX if its beta was 2 and the relevant risk free interest rate increased to 4%?

ke = rf + [expected return - rf] x β

ke = 4% + [12-4%] x 2 = 20%

The current risk-free rate is 5% and the expected market risk premium is 7%. CBF Ltd has a beta of 1.1.

Using the CAPM, what is CBF's cost of equity?

ke = rf + [expected return - rf] x β

ke = 5% + [7%] x 1.1 =12.7%

Cost of preference shares

P = Dp / kp (for non-redeemable preference shares, the cash flows are a perpetuity)

kp = Dp /P (rearranged for kp)

If annual dividends are $2 and the current preference share price is $35.

kp = $2/ $35 = 5.72%

If annual dividends are 10% of the $8 preference share issue price, and the current preference share price is $20:

kp = (10% x $8)/ $20 = 4%

C.2. Weighted average cost of capital

weighted average cost of capital

FRM Week 3 - Pre webinar activity

ZYX Ltd is financed by debt, preference shares and equity.

The book values and market values of each, and their respective market coats, are provided below.

What is ZYX Ltd's weighted average cost of capital?

weighted cost

debt: (2.4/8.8) * 4.5% = 1.23%

preference shares: (1.2/8.8) * 7.5% = 1.02%

equity: (5.2/8.8) * 16.5% = 9.75%

WACC = 12%

C.3. Weighted average cost of capital with taxes

maintain consistency both over time and between investments

align with cash flows (pre-tax v post-tax)

cost of debt is generally provided before tax

cost of preference share is generally provided after tax

cost of equity is generally provided after tax

convert to before tax: divide by (1 - tax rate)

convert to after tax: multiply by (1 - tax rate)

Comments