CPA FRM - Module 5: Interest rate risk management | KnowledgEquity

- Nov 19, 2020

- 7 min read

At the end of this module you should be able to:

explain what interest rate risk is

identify the sources of interest rate risk

evaluate the implications of interest rate risk management on cash flow

determine the key drivers that impact on interest rate risk management

evaluate the effectiveness and appropriateness of techniques to manage interest rate risk.

interest rate risks

borrowings: risk of rising interest rates

investment: risk of falling interest rates

assets/liabilities: fair value fluctuations

supply/demand: sales volume and value fluctuations

Carsales.com - interest rate risk

The Group's main interest rate risk arises from long-term borrowings. The Group's fixed rate borrowings and receivables are carried at amortized costs. They are therefore not subject to interest rate risk as defined in AASB 7 since neither the carrying amount nor the future cash flows will fluctuate because of a change in market rates.

Quiz. What does the RBA cash rate represent?

the bank bill swap rate (BBSW) 1

the 90 day bank bill futures 2

the overnight money market interest rate

the bank bill swap bid rate (BBSY) 4

BBSW: a short-term interest rate used a benchmark used for pricing securities. It is calculated and published by the Australian Securities Exchange (ASX). Typically the cash rate and BBSW rate are highly correlated.

90 day bank bill futures: a benchmark indicator for short interest rates and is traded at the ASX.

cash rate: the interest rate on unsecured overnight loans between banks. It is set by the Reserve bank of Australia (RBA).

BBSY: a benchmark derived from the BBSW and calculated as the average of the national best bid and best offer. It is usually 5 basis points above the BBSW.

Quiz. How is the RBA real cash rate calculated?

It is the difference between the cash rate and the BBSW

It is the difference between the cash rate and inflation

It is the difference between the cash rate and BBSY

It is the difference between the cash rate and the 90 bank bill futures

Quiz. Which three economies are included in the official policy interest rates of the G3?

Australia, China and the United States

The Euro area, Japan and the United States

Australia, the euro area and the United States

Interest rate drivers

central banks

G3 (forms the benchmark - US, Euro, Japan)

nominal vs real rate (nominal: stated rate, real: nominal - inflation rate)

Yield curve

normal yield curve: increases for longer maturities

inverse yield curve: decreases for long maturities

flat yield curve: remains the same

Interest rate risk management framework

1. set core criteria

role of the board

stakeholder expectation

internal operating environment

external operating environment

risk appetite

set by the board = management input + external environment

general policy - hedge strategy - liquidity risk - funding risk

establishing context

economic environment (yield curve)

organization culture

regulatory environment

competitors and substitutes

SWOT analysis

2. identify the exposures and sensitivities

timing mismatches

embedded options

offsets

commercial adjustments

Quiz. When the value of interest rate sensitive assets maturing in a given period exceeds the value of interest rate sensitive liabilities, what type of gap do we have?

positive (rate sensitive assets > rate sensitive liabilities)

negative (rate sensitive assets < rate sensitive liabilities)

neutral

Maturity profile and timing mismatches

identify maturity profiles for rate-sensitive assets/liabilities

plan ahead for rollovers, repayments and re-pricing adjustments

attempt to match their short-term assets with short-term liabilities, long-term assets with long-term liabilities

understand the effect of yield curves and interest rate movements

Offsets

Primary offset

organizations don't quickly jump into hedging interest rate exposures - they try as much as possible to offset exposure (by considering real derivatives, because they are cheaper than financial derivatives)

embedded options (CPI adjustments, on-charging, price limits)

e.g. if an organization is able to negotiate with a financial institution that if inflation rate increases then we will pass on this cost to the customer = primary offset

commercial (buying/selling, focus on margins, agreements/indexing)

diversification (portfolio theory, business unit exposures, centrally manage exposures)

e.g. Brazil might be operating in a very advanced economy as an example interest rates exposures or interest rates are very unfavorable but you might find that the in the case of Indonesia it could be the exact opposite and so when you bring these business units together you might find that is that our net worth between these organizations and so they the consolidated offset or the overall offset is actually less because of that portfolio because of that portfolio management of all these business units and

assets / liabilities

match your interest sensitive assets with your interest sensitive liabilities

investments

borrowings

Secondary offsets

financial instruments = expensive

Risk analysis

sensitivity analysis: how sensitive is the risk to movements

statistical analysis: what is the most likely outcome?

microsoft excel (goal seek, scenario manager, data analysis - e.g. regression)

3. appraise risks and set strategies

risk rating matrix

benchmarks

contingencies

Risk evaluation

based on likelihood of occurrence

based on impact or consequence

subjective, but aim to be objective

significance of rating determines action (& priority)

consequence table is very tailored to the organization

likelihood stable generally remains the same

Risk rating matrix

Targets and trigger levels

board will set benchmarks

return-based (e.g. ROA)

minimum product margins

trigger levels

determined by plotting potential outcomes

determining rates based on benchmarks

budget rate

minimum return

productivity bonus

Payoff diagrams

what is the current interest rate and cost?

plot the cost/return for rates above and below current rate

mark on Y-axis return target and minimum acceptable OR maximum acceptable cost and target

Timeframe for interest rate risk management (IRRM)

Life of the asset?

asset expired, debt repaid, cost of debt reset

but, hedging long-term assets is expensive

Variability of cash flows?

ability (inability) to pass on changes in interest rates

e.g. electricity retailer with limited pricing authority

Fixed/floating ratio

considerations:

organisation' financial strength

ability to accept/withstand volatility

competitor's hedging policies

board's risk appetite

covenants

financial ratios

meeting objectives

cost of capital

E.g. Fixed hedge ratios:

5 year period

60% fixed

- significant costs (normal yield curve)

- repricing risk (on eventual reset)

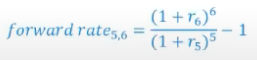

E.g. Forward rate calculation:

forward rate for 1-year in 5-years' time

= 3.4559%

r6: today's (spot) 6-year swap rate

r5 today's (spot) 5-year swap rate

the cost of hedging in a normal yield curve setting increases into the future

it is compensating for an extra 0.2% (approx) each year on the 6-year swap rate

4. manage risks

treasury operations

hedging

working capital management

contract management

manage/treat risk

retain risk

remove source

change the likelihood

change the consequence

pass it on

risk management strategies

reduce exposure

protect target profit

remove uncertainty

crisis protection

Quiz. CBF Ltd has $1 million in borrowings on a floating rate and wants to remove uncertainty relating to its exposure to interest rate movements. Which instrument would it use?

an interest rate cap option

a pay-fixed receive-variable interest rate swap

a receive-fixed pay-variable interest rate swap

interest rate swaps

fixed rate is the 'swap rate'

floating reference rate usually the BBSW (or LIBOR in overseas markets)

interest rate swap pay-off

fixed-rate payer = BBSW rate - Swap rate

floating-rate payer = Swap rate - BBSW rate

Company A wants to protect against interest rates rising on its variable (BBSW) borrowings of $500,000. Company A decides to fix the rate at 5.5% by entering into a fixed-for-floating interest rate swap with TYM Bank, with quarterly exchanges.

BBSW at the end of the June quarter is 5.75%

final cash flows for Company A

Company A interest owed on variable rate borrowings:

$500,000 x 0.0575 x (91/365) = 7,168

Swap payment received by Company A from TYM Bank (312)

Company A net interest on borrowings = 6,856

Effective interest rate = 6,856 / ($500,000*(91/365)) = 0.05500 = 5.5% = the fixed rate under the swap

Interest rate options

buying an option gives you a right

selling an option gives you an obligation

Caps

protect against rising interest rates

'capping' the interest rate (for borrowers)

buy an interest rate call option

the right to pay the cap (strike) rate at a future date

"long cap"

Floors

protect against falling interest rates

puts a 'floor' on the interest rate (for investors)

buy an interest rate put option

the right to receive the floor (strike) rate at a future date

"long put"

Which of the following would be the most likely reason for a company to enter into an interest rate collar option?

to cap the interest rate paid on borrowings at nil to minimal cost

to cap the interest rate paid on borrowings and make a profit on the option

to cap the interest rate paid on borrowings and benefit from any decrease in rate

Collars

used to decrease the cost of buying an option

buy a cap option to protect against rising rates

sell a floor option and receive a premium

right to pay the cap rate - pay premium

obligation to pay the floor rate - receive premium

E.g. protect against rising rates

sell a floor option (4%)

buy a cap option (6%)

BBSW = 4%

effective rate = floor 4%

BBSW < floor rate

effective rate = floor rate

BBSW = 7%

effective rate = cap 6%

BBSW > cap rate

effective rate = cap rate

BBSW = 5%

effective rate = BBSW = 5%

floor rate < BBSW < cap rate

effective rate = BBSW

Swaptions

an option to enter into a swap

payer swaption - pay fixed

receiver swaption - receive fixed

key points

if the swaption is "in the money", it will be exercised

e.g. for a payer swaption: if actual swap rate > swaption rate

ift he swaption is exercised then the swap will occur

otherwise, the swap does not occur

5. accounting and controls

reporting

governance

Accounting for interest rate risk products

derivatives must be recorded in the balance sheet at fair values (IFRS 9)

does the hedge qualify for hedge accounting?

e.g. eligible hedging instruments, eligible hedge items, formal designation, documentation and hedge effectiveness?

if yes, then fair value gains and losses can stay on the balance sheet until the underllying transaction is recorded in the P&L statement

Fair value

asset exchanged or liability settled

between knowledgeable, willing parties

arm's length, orderly transaction

present value of future cash flows

derivative fair values also incorporate counterparty credit risk

On 30th June 20X4, Wombat Pty Ltd entered into a fixed-for-floating interest rate swap on a notional principal of $1 million maturing on 30th June 20X9. Interest is calculated annually, with a fixed rate of 6% and a floating rate BBSW plus 1% margin.

You have been provided with the following market rate information as at 30 June 20X5 and requested to calculate the fair value of the swap.

Calculate the following amounts:

1. The discount factors that apply for each maturity date

= 1 / (1+4.5%)^(365/365) = 0.9569

= 1 / (1+4.75%)^2 = 0.9114

= 1 / (1+5.0%)^3 = 0.8638

= 1 / (1+5.5%)^4 = 0.8072

2. The 1-year forward rates that apply for each future period

= (DFnear / DFfar - 1) x (365 / d)

= ((0.9569/0.9114)-1) x (365/365) = 4.99%

= ((0.9114/0.8638)-1) x (365/365) = 5.51%

= ((0.8638/0.8072)-1) x (365/365) = 7.01%

3. The fair value of the swap

= PV of floating cash flows + PV of fixed cash flows

191120

Comments