university notes that's useful at work as a graduate accountant - P&L

- Aug 29, 2020

- 3 min read

FLIPPING HOUSE

Flipping: a term used primarily in the United States to describe purchasing a revenue-generating asset and quickly reselling it for profit.

Though flipping can apply to any asset, the term is most often applied to real estate and IPO.

RENTAL INCOME

Main residence exemption = exempt from CGT

Check agent statement

Land tax

Land tax online | Revenue NSW - Assessment calculation

Aggregated taxable land value 2,698,333

Less: threshold ( 629,000)

Tax $100 plus balance @ 1.6% 2,069,333 x 1.6% + $100

Total tax payable $ 33,209.33

Discount allowed (90.15) $ 33,119.15

Profit on sale of NCA

Tax reconciliation

NET PROFIT/LOSS PER THE ACCOUNTS

ADD: Taxable profit on sale of NCA

LESS: Accounting profit on sale of NCA

P&L

OTHER INCOME - Profit on Sale of Non-current Assets

BALANCE SHEET

Plant and Equipment

Motor vehicles - at cost 51,448 -> 0

Less: Accumulated depreciation (49,115) -> 0

Profit on sale of NCA 2,333

DR Profit on sale of NCA 2,333

DR Acc depreciation - motor vehicle 49,115

CR Motor vehicles - at cost 51,448

"GST you must pay when you sell property as part of your business."

Pre 01/07/2000: valuation method

Post 01/07/2000: consideration method

Example: Using the consideration method

Bob is a GST registered builder. On 1 December 2002, Bob purchased a block of land for $150,000 from a vendor who was not registered for GST.

Bob paid $550 in conveyancing fees and $7,000 in stamp duty on the purchase of the land.

Bob later constructed a house on the land and sold the house and land for $315,000. Bob chose to use the margin scheme to work out the GST on the sale.

The margin for the sale of the house and land package is $165,000 ($315,000 − $150,000).

The GST Bob must pay on the margin for the sale is $15,000 ($165,000 × 1/11th).

Bob has a tax invoice for the conveyancing fees and can claim a GST credit of $50 ($550 × 1/11th) in the tax period to which the purchase applies.

Bob also holds tax invoices for $110,000 of business purchases he made when building the house. Bob is able to claim $10,000 in GST credits for these purchases.

Bob is not entitled to any GST credits on the stamp duty as GST is not included in the cost.

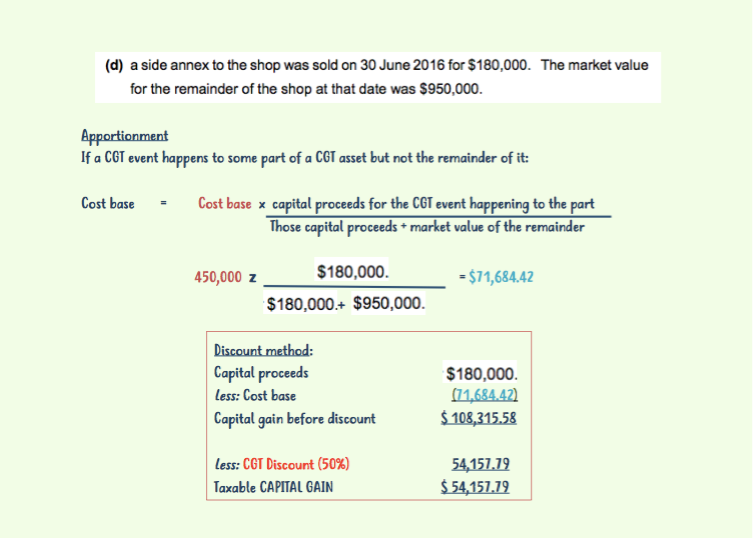

CAPITAL GAINS

sale of shares - REALISED

Taxable CG Calculation

CG not eligible for discount

Less: Capital loss _

A

Capital Gains eligible for discount

Less: remaining current year capital losses

Less: discount on eligible capital gains

B

Taxable CG (A+B)

Capital losses carried forward

sale of property - UNREALISED

Consideration

Less: agent commission

Less: legals Less:

Purchase price

Stamp duty

Legals

= Capital gains/Loss

Market value movement

Closing balance

Less: Opening balance _

Movement

Add: Proceeds from sales

Add: Disposal of revenue assets

Less: Purchases _

Total market movement

Realised market movement (accg cg)

Profit/loss on disposal of revenue asset

Unrealised market movement

Date: S3 2017

Subject: Revenue Law (BUSL320)

Description: Presentation on CGT

INSURANCE

Non-deductible insurance premiums include:

any insurance premiums paid by a non-complying SMSF

payments for insurance that covers events other than death, the existence of a terminal medical condition, or temporary or permanent disability (for example, funeral insurance).

Trauma insurance is non-deductible

Comments