CPA FRM - Module 6: Foreign exchange and commodity risk management | KnowledgEquity

- Nov 21, 2020

- 5 min read

At the end of this module you should be able to:

explain and calculate foreign exchange risk and discuss foreign exchange risk management

explain and calculate commodity price risk and discuss commodity price risk management

determine the key drivers that impact on currencies and commodity price risk management

identify and explain the sources of foreign exchange and commodity price exposures and sensitivities

analyse appropriate risk management strategies that address foreign exchange rate and commodity price exposures

select and apply appropriate hedging instruments to formulate strategies to manage foreign exchange and commodity price exposure.

Gold price exposure?

volatility?

gold price weakens?

Foreign exchange exposure?

functional currency?

AUD strengthens?

competitor position?

Hedging instruments?

forward contract?

futures? options? swaps?

Why only a portion?

level of sensitivity?

hope to achieve greater upside?

production estimates (impacted by weather, industrial action, etc)?

Part A: Foreign exchange risk

Risk of variation in exchange rates and the impact on an organisation - in terms of costs, revenues, assets, liabilities

Currency prices are highly volatile

Australian importers benefit from stronger AUD

Australian exporters benefit from weaker AUD

Hedging instruments

Forex forward (or future) - lock in rate

Forex swap - reduce exposure, provide certainty, or change cash flow timing

Forex option - limit exposure (cap, floor, collar)

A.1. Key elements of foreign exchange

spot price: how exchange rate is determined

two-way prices

forward rates

swaps

options

A.1.1 Spot price

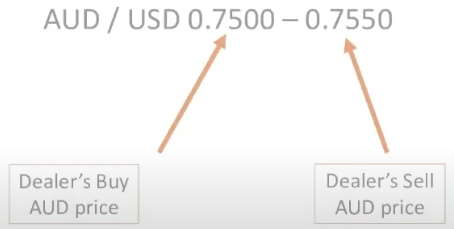

An Australian exporter wishes to sell 100,000 received from a sale and buy AUD. The exchange rate quoted by the bank is AUD/USD 0.7500 - 0.7525. How much will the exporter receive in AUD (in whole dollars)?

75,000

75,250

132,890

133,333

Dealer will buy AUD low/ sell AUD high

Buy AUD 1 for USD 0.75

Sell AUD 1 for USD 0,7525

= USD 100,000 / 07525

= AUD 132,890

A.1.2 Two-way prices

The following information is currently available:

current AUD/NZD spot rate 1.1200

NZ interest rate is 3% p.a.

Australian interest rate is 4% p.a.

What is the AUD/NZD forward rate in 180 days?

1.1092

1.1146

1.1254

forward price is not a spot rate forecast

It: interest rate of the terms currency

Ib: interest rate of the base currency

D: number of days from the spot value date to the forward value date

Y: number of days in the conventional year (e.g. US: 360 days, AU: 365 days)

Arbitrage

buying and selling an asset to make a risk-free gain based on pricing inefficiency

Assume the following:

AUD/EUR spot rate 0.5000

Australian interest rate 5.5%

Eurozone interest rate 3.0%

FX Dealer offers 1-year AUD/EUR forward rate of 0.4750 (based on a forecast)

Implicit exchange rate: EUR 10,300 / AUD 21,100 = 0.4882

A.1.4 Swaps

Swaps and timing mismatches

buy (sell) and sell (buy) and amount of currency on a date

exact reverse transaction on a future date

manages timing mismatches with FX cash flows

A.1.5 Options

Put

buy: right to sell at strike price

sell: obligation to buy at strike price

Call

buy: right to buy at strike price

sell: obligation to sell at strike price

FX put option - example

Fantell Ltd is an importer of manufacturing equipment. It has a large order that requires payment of USD $6,000,000 to its Japanese supplier in 3 months' time.

The current exchange rate is AUD/USD 0.8000 and Fantell Ltd wants to protect against a falling AUD. It decides to buy an AUD put option with a strike rate of AUD/USD 0.79000, for a premium of 0.0150.

Assuming the exchange rate in 3 months time is AUD/USD 0.7925, what is the AUD required by Fantell to settle the USD payment?

A.2. Foreign exchange risk management

FRM framework: https://angelaseoyeonlim.wixsite.com/angela/post/cpa-frm-module-5-interest-rate-risk-management-knowledgequity

A.2.1 Set the core criteria

Functional currency - different to reporting currency

Business drivers - profit targets, returns, cash flows, NPVs

Organisation objectives - strategic plans, opportunities and threats

A.2.2 Identify exposures and sensitivities

Committed - contracted (e.g. sales, purchases, interest payments)

Uncomitted - forecast transactions

Capital - assets, borrowings

Operating - revenues, costs, debt servicing

Primary - business operations

Secondary - result of hedging exposures

Transaction - paying or receiving foreign currency (Opex, Capex, Revenues)

Translation - Asset or liability in a foreign currency, Exposure impacts Balance Sheet

Competitive - competitor has a different (lower) cost base sourcing overseas

Apparent v Actual exposures

Internal offsets - e.g. exporting Product A- importing Product B

Embedded options - e.g. repricing clause in a purchase agreement

Timing mismatches - e.g. receipt of USD 5,000 today; payment of USD 5,000 in 3 months

Commercial adjustments - e.g. pass on costs to customer?

A.2.3 Appraise risks and set strategies

A.2.4 Manage risks

Foreign exchange risk

Forward exchange contracts

MNO Ltd is an Australian organisation that imports machinery from New Zealand. In 180 days, MNO Ltd is due to pay NZD 1,500,000 to a supplier.

The AUD/NZD spot rate is 1.1000. The AUD/NZD 180-day forward rate is 1.1027. An available AUD/NZD 6-month put option strike rate is 1.1100.

What is the AUD amount that MNO Ltd could lock in with a forward exchange contract?

AUD 1,351,351

AUD 1,360,297

AUD 1,363,636

AUD 1,654,050

Here, we can discard the reference to the spot rate and the available put option strike rate.

The AUD/NZD 180-day forward rate of 1.1027 would have been calculated using the forward rate formula. [The AUD is the base currency and the NZD is the terms currency.]

We need to apply this forward rate to the NZD 1,500,000 purchase price.

MNO Ltd can lock in AUD $1,360,297 (i.e. NZD 1,500,000 / 1.1027).

Forward exchange contracts

agreement with a bank

future dated

specified amount of currency

specified exchange rate

- no upfront costs

- calculated forward rate, not a forecast

- locked-in, no benefit from favourable movements

Forward exchange options

An Australian importer has a contract to purchase goods costing USD 50,000 in three months' time.

The current spot rate is AUD/USD 0.7500. To reduce exposure, an AUD/USD put option is purchased with a strike price of 0.7250 for a premium of 0.0050. If the exchange rate at expiration of the option is AUD/USD 0.7100, what is the importer's total cost in AUD?

AUD 66,667

AUD 68,965

AUD 69,444

AUD 70,422

(1) Exercise the put option as spot rate < floor rate at expiry

i.e. AUD/USD 0.7100 < AUD/USD 0.7250

(2) Adjust the effective exchange rate for the premium of 0.0050

i.e. AUD/USD 0.7250 - 0.0050 = AUD/USD 0.7200

(3) Sell AUD and buy USD at an 'effective rate' of AUD/USD 0.7200

= USD 50,000 / 0.7200

= AUD 69,444 [= 'total cost', including the premium]

FX options - usage

AUD put option = foreign currency call option

right to sell AUD and buy foreign currency

importer (limits losses on falling AUD, but retains upside)

AUD call option = foreign currency put option

right to buy AUD and sell foreign currency

exporter (limits losses on rising AUD, but retains upside)

Collar option

combination depends on requirements

nil or small premium (limits losses and limits upside)

A.2.4 Accounting and controls

Part B: Commodity price risk

Types of commodities

softs (grain, wheat, corn, etc)

precious metals (gold, etc)

base metals

energy

livestock

bulk (iron ore, etc)

Commodity basics

basic level goods (e.g. agricultural crops, metals, energy, livestock)

physical substances

quality unlikely to vary - but grades exist

Quiz. Contango and backwardation

The current exchange rate is AUD/USD 0.7500, and the 6-month forward exchange rate is AUD/USD 0.7700. The current crude oil spot price is USD 54.00 per barrel, and the 6-month crude oil forward price is USD 52.00 per barrel.

Which of the following correctly describes the crude oil market?

The crude oil market is in backwardation

In USD, the crude oil market is in contango

In AUD, the crude oil market is in contango

The crude oil price is going to fall in the next 6 months

USD:

Spot 54.00 > Forward 52.00

AUD:

Spot 54.00 / 0.7500 = AUD 72.00

>

Forward 52.00 / 0.7700 = AUD 67.53

Contango: forward price higher than spot price (price in future > today's price)

Backwardations: forward price lower than spot price

Quiz. Gold forward rate

Assume the following information:

Gold spot price is AUD 1,500 per ounce

Australian 12-month interest rate is 3%

12-month gold lease rate is 1%

Bank's profit margin is 0.50%

What is the effective gold forward rate in AUD?

AUD 1,500.00

AUD 1,522.50

AUD 1,537.50

Bank borrows an ounce of gold from the central bank and then raises AUD 1,500 per ounce by selling the gold on the spot market

Bank earns interest at 3.0%, offset by paying gold lease fees of 1.0% and taking a margin of 0.5%... the net benefit being 1.5% (0.030 - 0.015 = 0.015)

The effective gold forward rate is therefore AUD 1,500 x 1.015 = AUD 1,522.50

211120

Comments